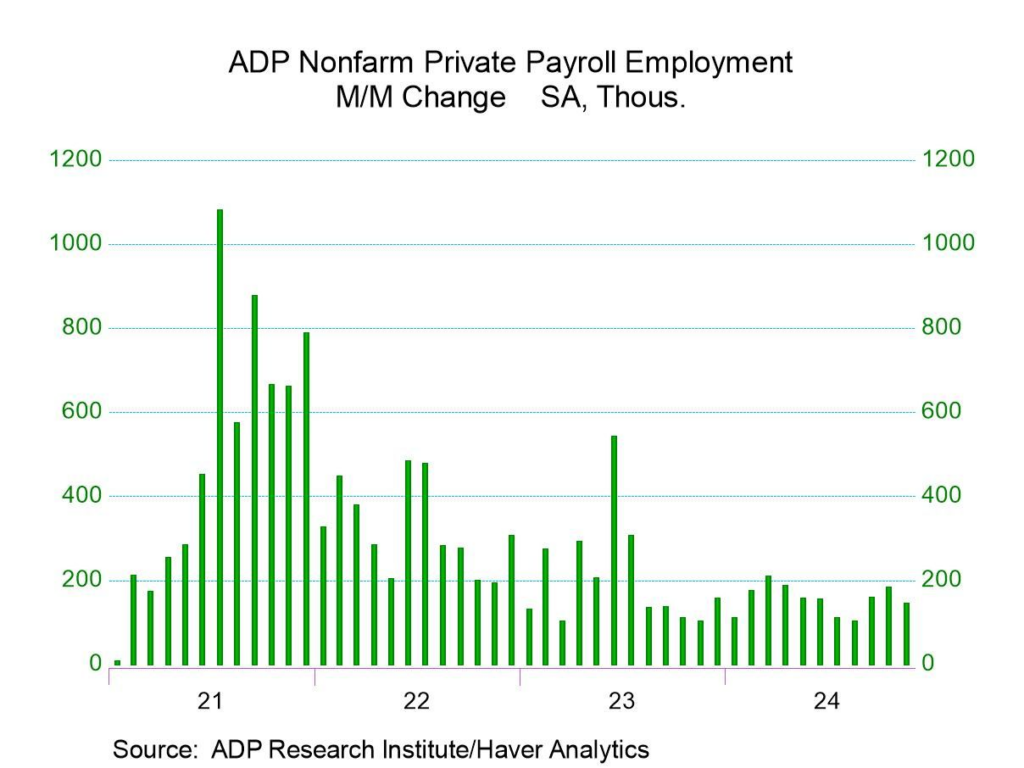

The U.S. private sector added 146,000 jobs in November, according to the latest ADP National Employment Report, which was released today.

This report, produced by ADP Research in collaboration with the Stanford Digital Economy Lab, also noted a 4.8% year-over-year pay increase for employees who stayed in their jobs. It marks the first uptick in over two years.

“Overall growth for the month was healthy,” said Nela Richardson, chief economist at ADP.

However, industry performance was mixed. Manufacturing, for instance, showed its weakest performance since spring. Financial services, leisure, and hospitality were also soft.

Large establishments led the job growth in November. Companies with 500 or more employees added 120,000 positions. Medium-sized businesses with between 50 and 499 employees contributed 42,000 jobs.

In contrast, small establishments with 1 to 49 employees saw a decline of 17,000 jobs. Notably, tiny businesses with 1 to 19 employees added 12,000 jobs. Yet, this gain was offset by a loss of 29,000 jobs among firms with 20 to 49 employees.

The service-providing sector dominated job growth, adding 140,000 positions. Educational and health services topped all sectors with 50,000 new jobs, reflecting the demand for healthcare and academic institutions.

Trade, transportation, and utilities added 28,000 jobs, buoyed by pre-holiday season activities. Other services, which include professions like repair and maintenance, posted a gain of 20,000 jobs.

Professional and business services added 18,000 jobs, which indicates steady demand for specialized services. Leisure and hospitality added 15,000 jobs, a modest increase suggesting tempered growth amid economic uncertainties.

Financial activities and the information sector grew by 5,000 and 4,000 jobs, respectively. Richardson noted that these sectors showed signs of softness.

In contrast, the goods-producing sector added just 6,000 jobs. Construction was bright, with 30,000 new jobs, likely motivated by continuous infrastructure initiatives and housing expansions.

Natural resources and mining added 2,000 jobs, maintaining a steady pace. However, manufacturing suffered a significant loss of 26,000 jobs, marking its weakest performance since spring.

The decline may be due to supply chain disruptions and decreased demand in specific manufacturing sub-sectors.

Job growth was uneven across U.S. regions. The South led with 61,000 new jobs, the South Atlantic states added 42,000, and the West South Central states contributed 30,000.

However, East South Central saw a decline of 11,000 jobs. The Northeast added 38,000 jobs. Middle Atlantic states experienced strong growth with 48,000 jobs. In contrast, New England states lost 10,000 jobs, indicating regional challenges.

The Midwest grew by 31,000 jobs. East North Central added 26,000 jobs, while West North Central contributed 5,000. The West saw an increase of 29,000 jobs. Mountain states added 18,000 jobs, and Pacific states grew by 11,000 jobs.

The report highlighted a notable acceleration in wage growth. Job-stayers saw their pay increase by 4.8% year-over-year, the first rise in 25 months.

Job changers experienced a pay gain of 7.2%, suggesting that switching jobs continues to offer significant financial benefits.

Industry-specific wage gains for job stayers varied. Construction workers enjoyed the highest pay increase, at 5.2%, while education and health services employees saw a 5.1% raise.

Monetary operations, recreation, tourism, and additional services each reported a 4.9% increase. Manufacturing workers received a 4.7% raise despite the sector’s job losses. Natural resources and mining had the lowest wage growth at 3.6%.

Wage growth by firm size also showed interesting trends. Employees at small firms with 1 to 19 employees saw pay increase by 4.2%, and those at small firms with 20 to 49 employees saw a 4.8% wage growth.

Medium firms with 50 to 249 employees gave employees a 4.9% pay raise. Medium firms with 250 to 499 employees saw wages grow by 4.8%. Employees at major companies with 500 or more staff members experienced a 4.7% increase.

The mixed performance across industries and regions suggests a nuanced economic landscape. The significant job losses in manufacturing could signal broader economic challenges, affecting supply chains and export dynamics.

Robust education, health services, and trade growth indicate sustained consumer demand. It also shows resilience in essential services.

The acceleration in wage growth may contribute to inflationary pressures. It poses challenges for policymakers who must balance economic growth and price stability.

The decline in employment among small establishments highlights these businesses’ vulnerabilities amid economic fluctuations.

Economists closely watch these trends for signs of how the labor market might evolve.

“The increase in wage growth, especially among job-stayers, could indicate that employers are raising wages to retain talent,” said Dr. Laura Martinez, an economist at the Economic Policy Institute.

James Thompson, a senior analyst at Capital Economics, added insights.

“The divergence between large and small businesses in job creation is significant,” he said.

Large companies may have more resources to expand and hire, while small businesses could grapple with higher costs and uncertainties.

Various factors will influence the labor market’s trajectory. Monetary policy may consider these employment and wage trends when deciding interest rates. The Federal Reserve aims to curb inflation without stifling growth.

December’s data will reveal how the holiday shopping season affects employment, particularly in retail and logistics. International trade dynamics and geopolitical events could impact manufacturing and other export-dependent sectors.

It’s important to note that the October job gains were revised downward from 233,000 to 184,000. The report mentioned that the November employment estimates are informed by the latest Quarterly Census of Employment and Wages data, which influenced the revision.

An annual benchmarking of the entire data series is scheduled for the January 2025 release.

The ADP National Employment Report is a separate assessment that provides a high-frequency view of the private-sector labor market. It is derived from accurate, anonymized payroll information of over 25 million employees in the U.S.

It offers insights into employment changes across industries, regions, business sizes, and pay trends.

The December 2024 ADP National Employment Report will be released at 8:15 a.m. ET on January 8, 2025. For more detailed information and interactive charts, visit the ADP National Employment Report website.